Being financially honest

A lot of us know that feeling: We work hard, we make a salary that should be plenty, but somehow the balance on our savings never get really high. Or you're interested in buying a home and need to save up at least 3.5% for an FHA loan, plus the money you need to move and install a secret door.

I've never done any budgeting, and the amount of financial planning I did was mostly "Make sure the checking account has always enough balance for the next rent, and that the credit card never exceeds what I can pay back at the end of the month". After all, finance is booooooring. For me, there was an extra difficulty as I'm an immigrant to the USA and just didn't know much about money in this country. The 2008 crash didn't help spark my interest either (my #1 priority: Make sure the money is FDIC insured).

Boy, if I could go back to when I first arrived here and I could only tell my past self one thing, then it's to be a bit more financially honest and save money. Oh, and pick up a copy of Get a Financial Life, it's an awesome, not dry overview of the stuff that matters. And for god's sake, don't wait four years to setup a 401(k).

For the past few months, I've been using You Need A Budget (YNAB) to get an overview about where my money goes. They have a Four-Rule-Methodology, which is useful if you need to control your spending and want to make a household budget, but I've been using it as a reporting tool to get a feel for it. The general idea is that you add your accounts (Checkings, Savings, Credit Cards, Loans, ...) and assign each transaction a category of your choice.

This takes a few hours when you're just starting out - most banks and credit cards should offer a Quicken (.qfx) or CSV Export, which you can mass-import into YNAB. You'll be creating and tweaking categories (e.g., I have categories based on different hobbies) and assign all your transactions to it. I recommend starting small, with just the info from last month and then adding more and more to it if you want. The more data you have, the better reporting is, but the longer it takes to setup.

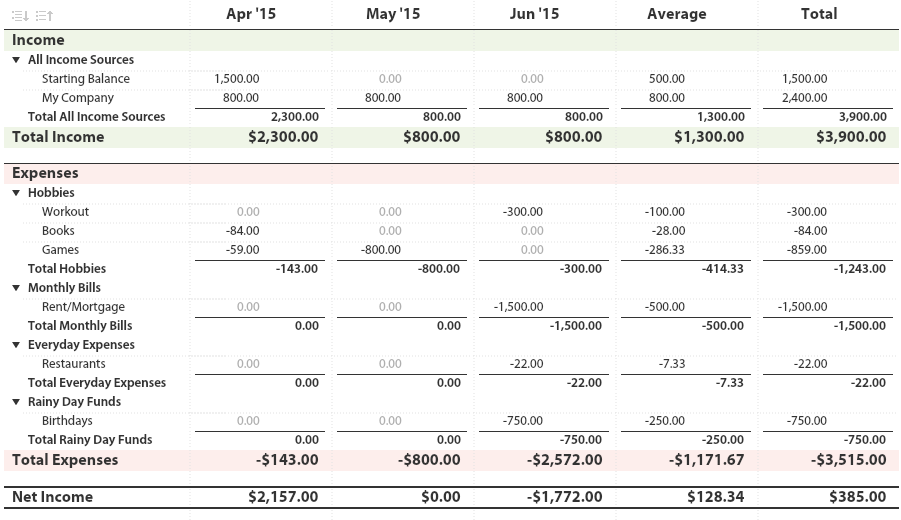

Once your transactions are in and categorized, you can report on it. This is where we're getting serious because now you're really seeing how much all these little $4.99 purchases add up to.

Clicking on a category allows you to dig in or see which transactions are part of this.

This is pretty eye-opening, but if you need some more motivation there is a handy Income v. Expense report. If you manage to have an entire year of transactions, this report can be pretty disturbing - it's an honest, no-BS assessment of your financial discipline.

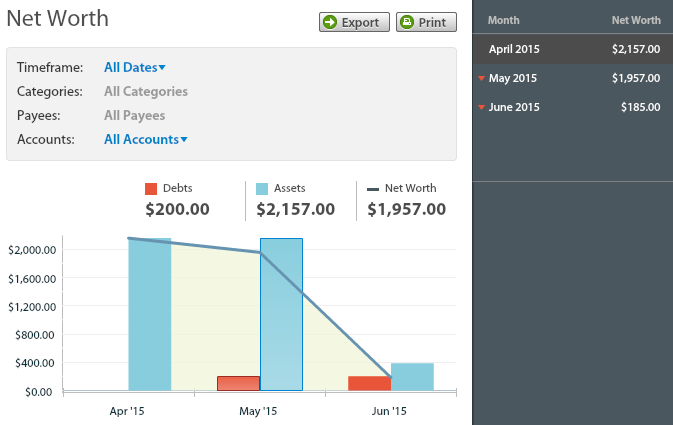

YNAB also supports Debt-Accounts, like Credit Cards or Loans, and a Net Worth graph.

I'm not going much into the Budgeting features of YNAB - it's arguably the feature it advertises the most, but it's also the thing that takes effort. If you don't have anything right now, then just going in and using it for reporting will be a huge eye-opener already.

When it comes to money, it is important to be honest to yourself - it's okay to spend thousands of dollars on your hobby, as long as you know that's where the money goes and don't end up at the end of the year looking at a zero-sum game and an emergency fund that is still empty.